This is another my favourite brand, i love their milk and yogurt drink and been drinking their milk since i dont know, maybe since i start loving milk. :p

The commodity price really hurt their Q4 earning, plus, like previous year Q4 sales normally lower than Q3. Looking at recent milk powder price trend, seems like their margin going to depress for next few months and they need to push for more sales in order to avoid slower net profit growth.

Overview of Milk industry (Dairy Commodity)

i) Global dairy product demand has increased. In particular, Asian nations’ improving economies have created desires for better, Western-style foods (more meat, more dairy). China’s basic food needs are drought-stressed.

ii) New Zealand’s milk output has been challenged by adverse weather.

iii) The U.S. dollar’s value has slumped, making foreign purchases of U.S. goods relatively cheaper.

iv) U.S. exporters (particularly cooperatives) have been giving away dairy products at prices far below global market values

Unlike automotive industry, normally they can pass a bit the impact to end user, which is us, the customer. Luckily my ex manager (my favourite boss of all time) currently managing the cost there, i might get some insight on the raw material & cost impact, if i decide to switch my other stock to DLADY. According to him, only special ingredient is imported from Netherlands, the rest mostly locally produced (the dairy product). Overall, Dlady managed to post a growth in sales in net profit FY2010.

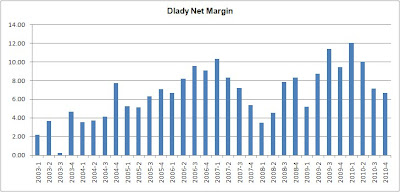

In past 5 years, the lowest margin was 5.99%, back in 2008. Assuming that they manage to post small growth at 2.7% with net margin est at 6.5% (being defensive here), the est EPS would be 0.86. At current price of RM15.50, the forward PE ratio would be >18. Expensive!

Going forward, i think its worth to buy and hold as always reward a steady dividend to shareholders.But not at current price of course. Maybe below than RM15.00??

Dutch Lady PATMI (quarterly)

Dutch Lady Revenue (quarterly)

Dutch Lady EPS and Gross DPS